Share this

Use Your Data to Get Proactive

Use Your Data to Get Proactive

April 16, 2021

1

min read

Go for Gold: Help Your Team Achieve Peak Performance with Property Hub

Go for Gold: Help Your Team Achieve Peak Performance with Property Hub

August 19, 2024

3

min read

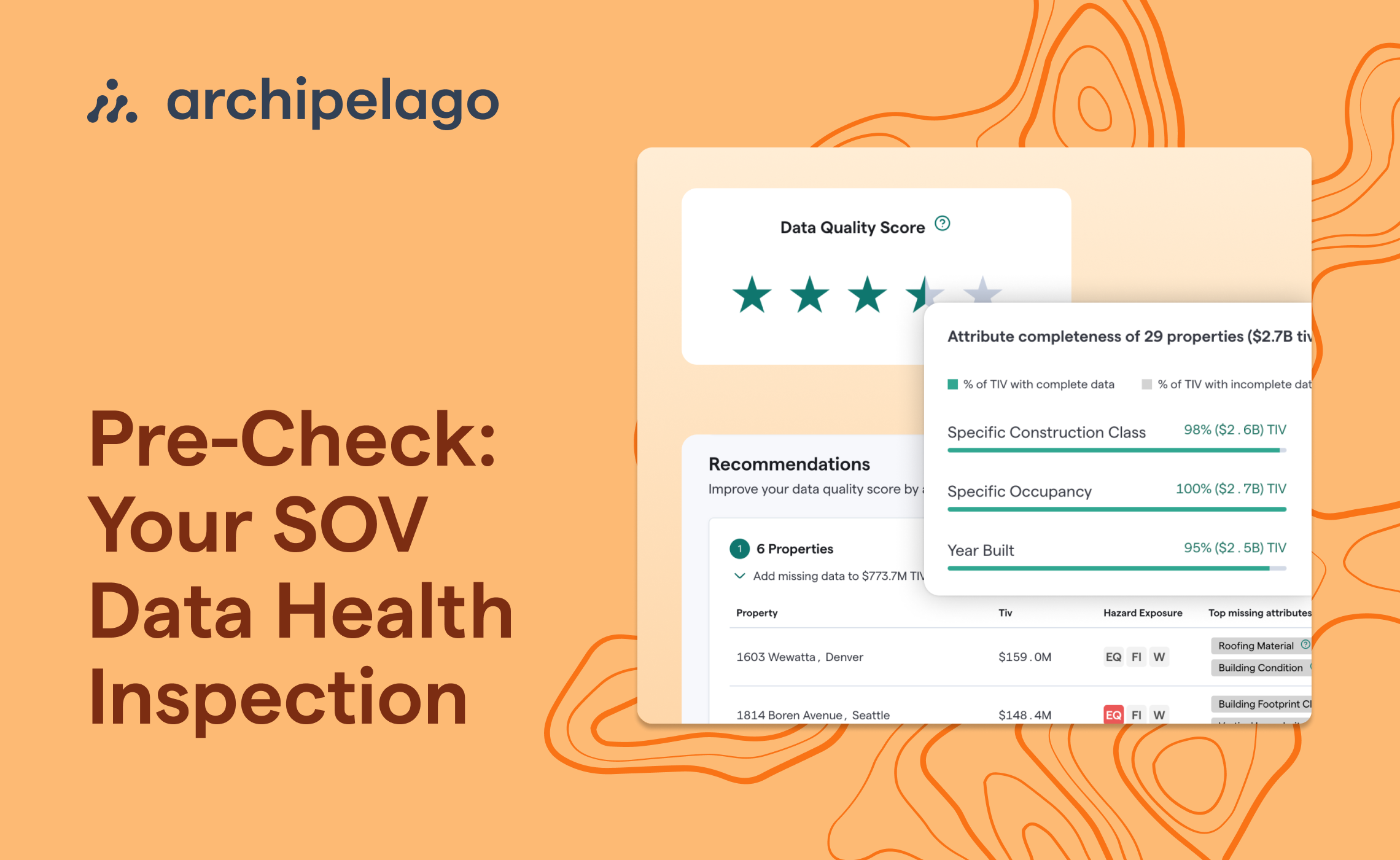

Pre-Check: Your SOV Data Health Inspection

Pre-Check: Your SOV Data Health Inspection

July 26, 2024

4

min read